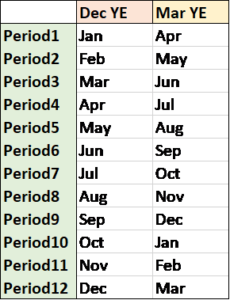

Multi-calendar reporting is a common Financial Reporting requirement where the fiscal year ends for submitting entities are different than the consolidated group or intermediary sub-group fiscal year end. For example, the consolidated group fiscal year end could be December 31 while some submitting entities or intermediary sub-groups have a March 31 or June 30 fiscal year end.

Multiple fiscal year ends often arise for organizations that are highly acquisitive (mergers, acquisition, divestures) or geographically dispersed (e.g., for tax efficiency purposes).

Multi-calendar reporting is not an Out-Of-The-Box (OOTB) feature for Oracle Financial Consolidation and Close (FCC) nor most financial consolidation platforms for that matter, in this article, we will cover how you are able to achieve this in FCC with the proper configuration and set up.

The following is a high-level summary of how we were able to set this up for one of our clients.